The Markets:

After

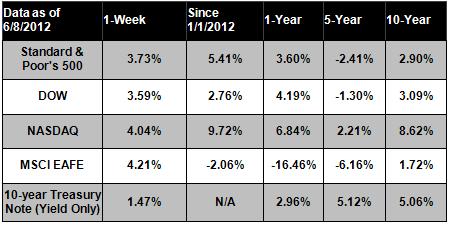

the sustained selloff in previous trading sessions, the markets rallied

Friday to claim a strong gain for the week. The S&P and Dow both

booked a 0.8% gain, while the Nasdaq rose 1.0%.[1]

With the choppy market performance and gloomy economic sentiment we've

seen in the past weeks, we wanted to spend some time discussing recent

trends and what they might mean for the future.

In

short, many of the problems that plagued the markets in 2010 and 2011 -

a serious European debt crisis and recession, a slowing Chinese

economy, slow domestic growth, and the looming expiration of Bush-era

tax cuts - are still with us in 2012. The uncertainty around these

issues has dealt investor sentiment a major blow and spurred an exodus

from equities into bonds and other "safe haven" investments, pushing

Treasury yields to record lows similar to levels seen in the 2008

crisis. There's a real current of fear underlying these moves that the

global economy is slipping back into recession.

Whether

this fear is realized depends largely on how the credit crisis in Europe

develops. Things may be looking up (at least temporarily) as Eurozone

leaders have pledged to lend Spain up to 100 billion euros (approx. $125

billion) to recapitalize its banks, pending an audit this month. By

pumping more liquidity into the economy, policymakers have bought

themselves a bit more time to find a solution.[2] We hope that markets will react positively to the news this week.

Domestically,

many people are worrying about whether 2012 will be a repeat of the

last two years, where an initially promising start fizzled out in the

spring. Economic data has been patchy at best, and employment growth

seems to have lost steam over the past few months, with not nearly

enough jobs created to sustain continued growth. At this point, we can't

be sure if this is just a temporary slowdown or a sign of continued

economic contraction. Based on a number of factors, we currently suspect

that this is a temporary, cyclical slowdown and that job growth will

pick up in the latter half of the year. Supporting this belief, the

Fed's most recent Beige Book report stated that U.S. economic growth

picked up over the last two months, and hiring showed signs of a "modest

increase," indicating that the situation is not as grim as many

originally feared.[3]

With

respect to equity markets, we know that historically, the market

suffers one 10% (or greater) market correction each year. The S&P

briefly touched an intraday correction of 10%, so does that mean we can

expect solid growth going forward? It's impossible to know for sure, but

it's rare to see the kind of persistent selling pressure that we've

seen for the last month, where, for example, the Dow experienced 17

losses in 22 trading sessions. This lingering weakness has resulted in

very pessimistic investor sentiment that may set markets up for a

positive rebound. Additionally, we're also under the effect of typical

Presidential Election year trends, which historically have called for a

peak in April and a decline in June, a script the markets have followed

closely this year. If the cyclical trend continues, we can expect a new

burst of energy in the second half of the year.

ECONOMIC CALENDAR:

Tuesday: Import and Export Prices, Treasury Budget

Wednesday: Producer Price Index, Retail Sales, Business Inventories, EIA Petroleum Status Report

Thursday: Consumer Price Index, Jobless Claims

Friday: Empire State Mfg. Survey, Treasury International Capital, Industrial Production, Consumer Sentiment

|