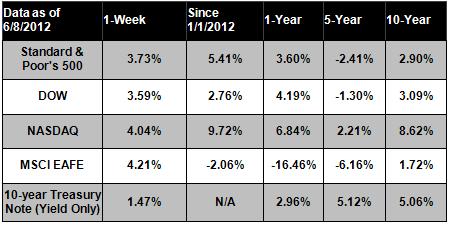

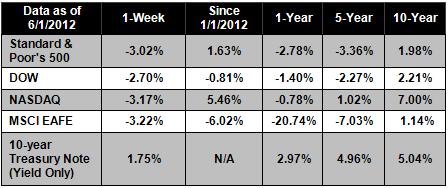

THE MARKETS - Weekly Update - June 4, 2012

Gloomy economic data disturbed markets last week and set off alarm bells that the U.S. economy may be following Europe and Asia into a slowdown. Friday's grim jobs report showed that the economy added just 69,000 new jobs in May, far below consensus estimates, and the unemployment rate rose to 8.2% from April's 8.1%. Equity markets tumbled on the news, and the Dow showed its worst performance of the year, dropping 2.70%, while the S&P and Nasdaq lost 3.07% and 3.17%, respectively.[1] The Dow Jones Industrial Average has now slipped into negative territory for the first time in 2012, exactly one month after closing at a multi-year high.[2] Meanwhile, the S&P 500 is still up 1.6% year-to-date, and the Nasdaq Composite is up 5.5%.

Earlier in the week, the first quarter GDP growth estimate was revised downward to 1.9%, from the 2.2% originally reported. Although analysts had initially expected GDP growth of at least 2% in 2012, that number is beginning to look overly optimistic. Revisions to reported estimates are worth paying attention to because they can serve as leading indicators of which direction the economy is going next.[3] The jobs data is troubling and has potential to further stall the economic recovery. Rationalizations that a warm winter artificially shifted job growth earlier in the year appear increasingly thin. The job market is simply not growing enough to ignite a robust recovery.

Thankfully, the economy is still resilient in some areas. Inflation remains reasonably low, auto sales have continued to grow, and falling energy prices are easing the strain on consumer pocketbooks, opening the door to increased consumer spending. Even so, some analysts believe that we are falling into a familiar pattern where the economy gains traction early in the year only to falter in the second quarter. With both perspectives in mind, it would be premature to predict which way things will move next. Interestingly, in 2011, the Dow's first close in negative territory for the year was on August 4th, but the year still ended with a 5.5% gain.[4]

While it's hard to dredge up the fortitude to stay invested when faced with such a slate of bad news, we haven't yet seen the effects of lowered gas prices on consumer spending, and the U.S. is still much better off than Europe. We live in a dynamic economic system; when one asset class goes down, another comes up. We can't predict the future, but we should always continue looking for opportunities!

Notes: All index returns exclude reinvested dividends, and the 5-year and 10-year returns are annualized.

Sources: Yahoo! Finance, MSCI Barra. Past performance is no guarantee of future results.

Indices are unmanaged and cannot be invested into directly. N/A means not available.